Gen Z is emerging as the fastest-growing and most dynamic segment in the Canadian credit market, according to TransUnion's Q1 2026 Credit Industry Insights Report. The number of credit-active Gen Z consumers increased by more than 460,000 year-over-year, a 7.8% rise, outpacing all other generations. Average non-mortgage balances for Gen Z rose 9.1% to $13,621, also the highest growth among age groups.

Credit Demand and Supply Trends

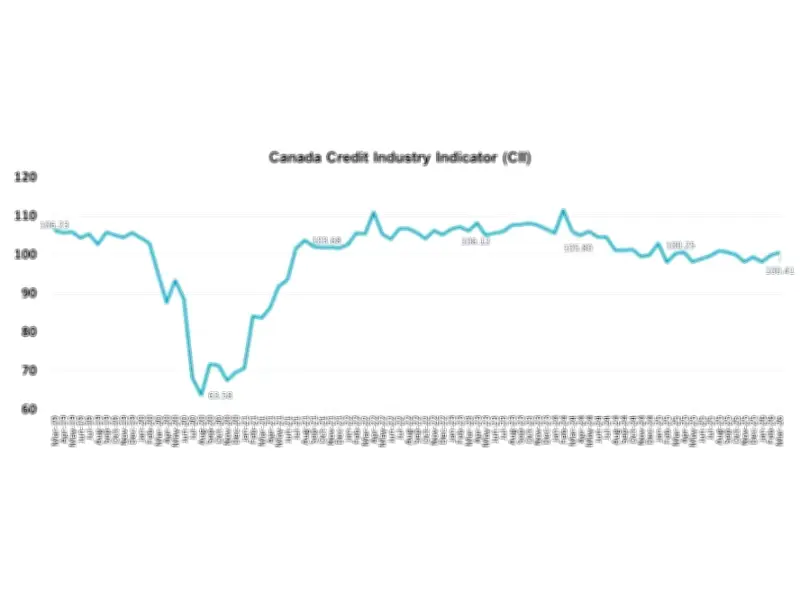

TransUnion's consumer credit index remained flat year-over-year, reflecting a slow long-term decline. However, Gen Z's increasing participation and higher credit utilization indicate a shift beyond early adoption toward expanded wallet profiles with additional products like credit cards, personal loans, and secured loans such as auto loans and mortgages.

Overall, non-mortgage balances per consumer grew across most generations: Millennials saw a 6.1% increase to $29,747, Gen X rose 2.4% to $42,226, while Baby Boomers and the Silent Generation experienced slight declines of 0.2% and 0.6%, respectively.

Delinquency Stabilization and Regional Variations

Delinquency rates showed signs of stabilizing during a period of relative economic stability. Mortgage balances continued to climb, while delinquency rates returned to pre-pandemic levels. Regional trends highlight diverging risk profiles across provinces, though the report did not provide specific provincial data.

Gen Z consumers improved their credit performance across all delinquency levels over the past year, meaning fewer fell behind on payments. However, they still had the highest incidence of delinquency compared to other generations, attributed to shorter credit histories and thinner credit files. Only 19.9% of Gen Z are considered super prime, versus 42.2% of the total population.

Borrowing Patterns and Future Outlook

Recent borrowing patterns among Gen Z reflect demand for accessible funding, streamlined approvals, and flexible repayment options, suggesting increased use of credit for day-to-day expenses. Older Gen Z consumers are beginning to enter secured loans like auto loans and mortgages. Although Gen Z currently carries lower overall debt on average, balances may grow as more consumers enter the market and progress through life stages.

TransUnion noted that Gen Z has potential for future score improvements and broader access to credit products over time, as demonstrated by prior studies. The report underscores the dynamic nature of the Canadian credit market, with Gen Z driving growth while overall delinquency trends stabilize.