Global supply chains remain under significant strain as manufacturers front-load purchasing to guard against anticipated higher prices in the second half of 2026, according to the latest GEP Global Supply Chain Volatility Index.

Key Findings from May 2026

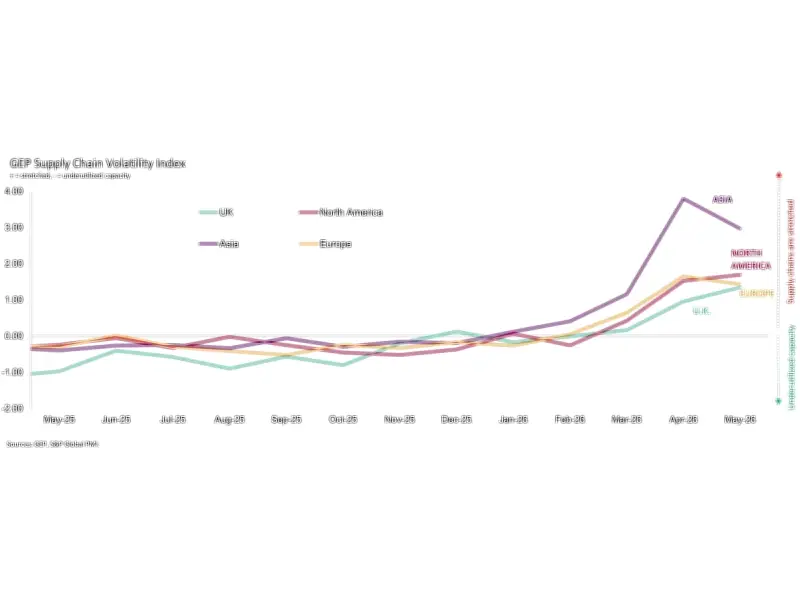

Safety stockpiling, shortages and transportation costs have all been elevated for three consecutive months, a rare signal outside the 2021-23 supply chain crisis. The index, based on a monthly survey of 27,000 businesses, shows that North America supply chain pressures rose to their highest level since August 2022, while Asia remains under the greatest strain globally.

Stockpiling and Shortages Worsen

Reports of safety stockpiling rose to their highest level since January 2023, as companies bulk ordered goods and raw materials ahead of expected price increases and potential supply disruption. This front-loaded purchasing pushed global demand for inputs to its strongest since March 2022. Shortages also worsened in May, reaching their highest level in three-and-a-half years. Combined with elevated transportation costs, the data shows that supply chain pressures are no longer limited to shipping and energy markets.

May's data also points to a rare pattern: for three consecutive months, stockpiling, shortages and transportation costs have all been elevated. Outside the 2021-23 supply chain crisis, this has typically been followed by a sharp fall in the index as supply chains self-correct, often through weaker input demand or deteriorating economic conditions.

Expert Commentary

"The path for inflation is already being set, and companies are trying to limit the damage," said John Piatek, vice president, consulting, GEP. "The surge in purchasing we saw in April and May is likely temporary. Once companies have built inventory, they and their customers will pull back, which means supply chain pressures may ease. But, even if the Strait of Hormuz is opened fully, economic conditions will likely weaken in the second half of the year as companies will pull back on their input purchasing to draw down the inventories they've built up."

Regional Breakdown for May 2026

- Asia: Index fell from 3.79 to 2.96, signaling a slight easing of pressures versus April. Nonetheless, the index was indicative of significant supply chain stress for Asian manufacturers.

- North America: Index rose to 1.69, from 1.52, its highest level since August 2022. Stronger purchasing activity, particularly in the U.S., and greater stockpiling drove the rise in supplier capacity pressures.

- Europe: Index fell to 1.43, from 1.64, as factory purchasing volumes across the continent were tapered. This reflected fresh signs of weakness in the German and French manufacturing economies.

- United Kingdom: Index rises to a three-and-a-half year high of 1.34, from 0.96 in April, pointing to greater capacity constraints for suppliers used by U.K. manufacturers.

Interpreting the Data

Index > 0: Supply chain capacity is being stretched. The further above 0, the more stretched supply chains are.

Index < 0: Supply chain capacity is being underutilized. The further below 0, the more underutilized supply chains are.