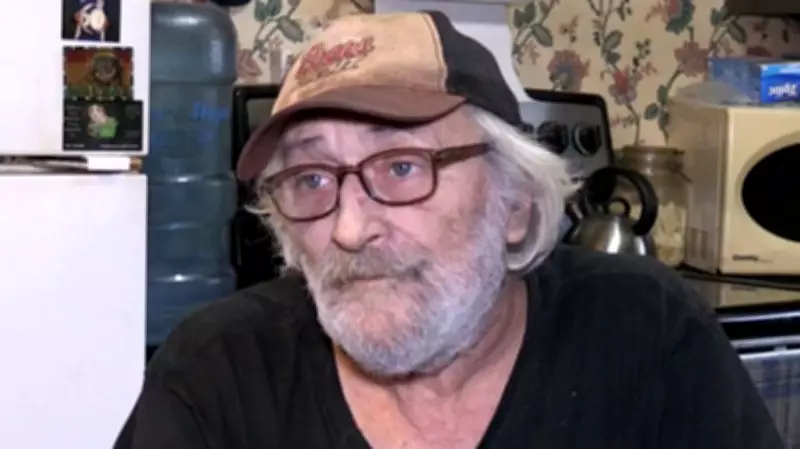

An Ontario man has been struggling to repay a $4,500 loan for the past five years, with his payments barely making a dent in the principal due to exorbitant interest rates. The case highlights the ongoing issue of predatory lending, even as new regulations aimed at curbing such practices came into effect in 2025. However, these rules do not apply to pre-existing high-interest loans, leaving many borrowers trapped in cycles of debt.

Consumer Alert: Predatory Lending Loophole

Pat Foran reports on the plight of one individual who took out a $4,500 loan but has been unable to significantly reduce the balance despite years of payments. The borrower expressed frustration, stating, 'No possible way to pay this.' The situation underscores the challenges faced by consumers who entered into high-interest agreements before the new regulations were enacted.

New Rules, Old Problems

The Canadian government introduced stricter rules on predatory lending in 2025, including caps on interest rates and fees. However, these measures do not apply retroactively, meaning existing loans continue to accrue at previously agreed-upon rates. Consumer advocates argue that a transition period or retroactive application is necessary to protect vulnerable borrowers.

- High-interest loans can trap borrowers in debt cycles.

- New predatory lending rules took effect in 2025 but exclude pre-existing loans.

- Consumer advocates call for broader protections.

Impact on Borrowers

The Ontario man's experience is not unique. Many Canadians with high-interest loans face similar struggles, often paying more in interest than the original loan amount. Financial experts advise borrowers to seek credit counseling or explore debt consolidation options, though these may not be accessible to everyone.

For more information on predatory lending and consumer rights, visit the Financial Consumer Agency of Canada website.