As the holiday season approaches and financial pressures mount for many Canadians, buy now, pay later services are becoming increasingly attractive options for budget-conscious shoppers. These short-term payment plans promise immediate gratification with delayed financial consequences, but experts warn they can quickly spiral into overwhelming debt without proper understanding and planning.

The Different Faces of BNPL Services

Buy now, pay later arrangements have existed in various forms for decades under different names including retail financing agreements, credit card installment plans, and retail credit services. Despite the branding differences, they all provide the same fundamental service: allowing consumers to purchase products immediately while postponing payment.

The traditional deferred payment model typically links to specific store credit cards featuring "no payments, no interest" promotions, commonly used for furniture, appliances, or electronics purchases. While some plans require payments during the interest-free period, most allow complete payment deferral until the promotional period concludes, provided the full balance settles before the deadline.

Credit card installment plans represent another variation, enabling cardholders to convert eligible purchases or portions of their balance into structured loans with fixed monthly payments. These arrangements often feature lower interest rates than standard credit card balances, though they may include setup fees. The critical risk involves missing payments, which can terminate the favorable terms and revert to higher interest rates.

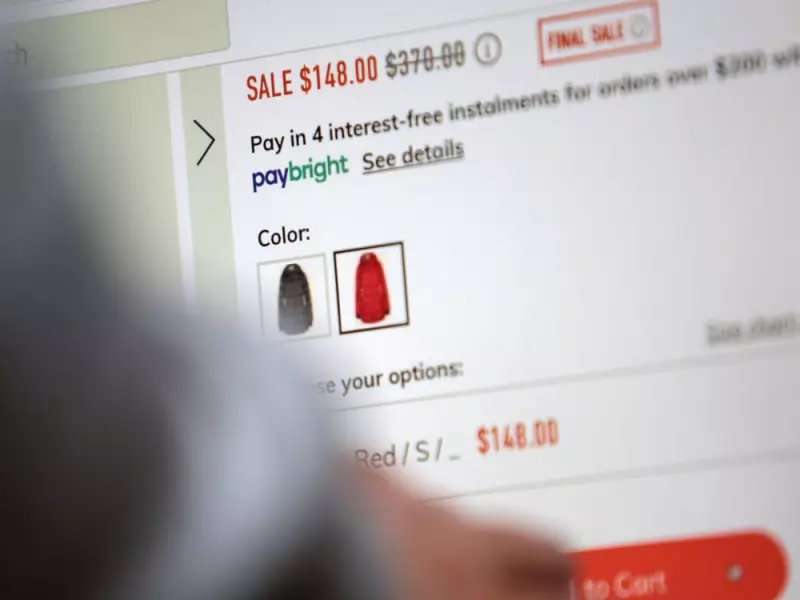

The Modern BNPL Revolution

Today's most popular BNPL options appear directly at checkout counters, both online and in physical stores. Services like Klarna, Afterpay, Affirm, Sezzle, and PayPal's Pay in 4 typically divide purchases into three or four equal monthly installments.

Approval processes generally involve soft credit checks that don't impact credit scores, followed by authorization for automatic deductions from bank accounts or credit cards. When used with careful budgeting, these services can provide legitimate benefits by distributing larger expenses across multiple pay periods.

Weighing the Benefits Against the Risks

The convenience of BNPL services has exploded in popularity since the pandemic, offering flexibility for managing significant or unexpected expenses without accumulating credit card-level interest charges. These plans can effectively help consumers schedule payments for planned purchases when accompanied by solid repayment strategies.

However, the dangers become apparent when users lose track of multiple BNPL agreements, each with distinct terms, conditions, and repayment schedules. Without clear organization and budget allocation for upcoming payments, what begins as financial convenience can rapidly transform into unmanageable debt.

Financial experts emphasize that while BNPL services offer temporary relief during expensive holiday seasons, they require the same disciplined approach as traditional credit. Consumers should carefully review all terms, set reminders for payment dates, and ensure they have adequate funds available before committing to multiple installment plans simultaneously.